JHVEPhoto

Earnings of United Bankshares, Inc. (NASDAQ:UBSI) will most probably dip this year on the back of a fall in mortgage banking income. Further, higher provisioning will likely drag earnings. On the other hand, mid-single-digit loan growth and slight margin expansion will support the bottom line. Overall, I’m expecting United Bankshares to report earnings of $2.50 per share for 2022, down 12% year-over-year. Compared to my last report on the company, I’ve tweaked downwards my earnings estimate mostly because mortgage banking income missed my expectations for the first quarter of the year. The December 2022 target price suggests a small upside from the current market price. Therefore, I’m maintaining a hold rating on United Bankshares.

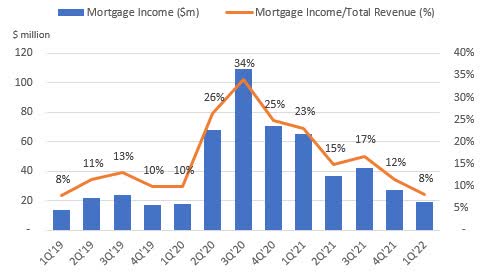

Mortgage Banking Income Has Normalized Faster than Expected

Mortgage banking income for the first quarter of 2022 dipped by more than I expected. In fact, United Bankshares’ non-interest income for the first quarter of 2022 almost halved from a year ago period. During the first quarter, mortgage banking income dropped to the level of the pre-monetary-easing cycle, as shown below.

SEC Filings

Therefore, it seems like the party ended sooner than I expected. With interest rates set to continue to rise, mortgage banking income will likely remain stable at the first quarter’s level throughout the remainder of the year. Meanwhile, other fee income will likely continue to grow at a normal rate.

Overall, I’m expecting United Bankshares to report a total noninterest income of $205 million for 2022. In my last report on United Bankshares, I estimated a noninterest income of $259 million for 2022. I have reduced my estimate mostly because of the first quarter’s surprise.

Loan Growth to Decelerate but Remain Moderately High

United Bankshares’ loan growth continued to remain strong in the March-ending quarter, for a second consecutive quarter. As mentioned in the earnings presentation, loan pipelines continued to remain very strong at the end of March 2022. Therefore, similar performance can be expected for the second quarter of the year. However, loan growth will likely slow down in the second half of the year because of rising interest rates that will dampen credit demand. The demand for residential mortgages will likely be the most affected by higher interest rates.

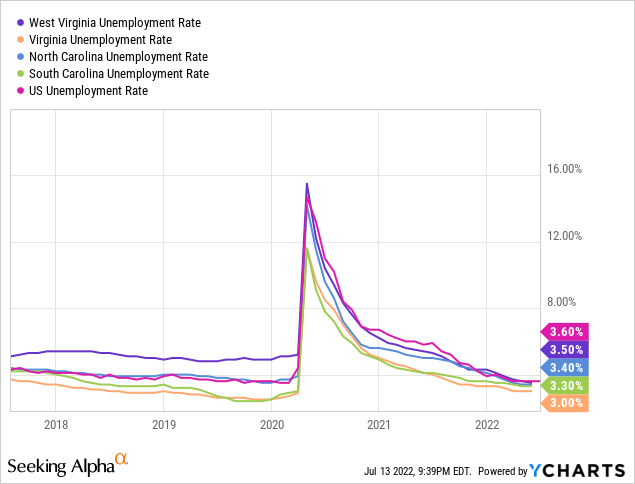

On the other hand, strong job markets will likely support loan growth. United Bankshares operates in West Virginia, Virginia (including Washington DC), North Carolina, and South Carolina. All these states have stronger job markets than the national average, as shown below.

The management mentioned in the presentation that it expects mid-single digit loan growth for the last three quarters of 2022. Considering these factors and management’s guidance, I’m expecting the margin to increase by 6.0% by the end of 2022 from the end of 2021. The acquisition of Community Bankers Trust (ESXB) on December 3, 2021, increased the loan portfolio size by around $1.3 billion. Due to the timing of the acquisition (late 2021), the average loan balance for 2022 will be much higher than the average balance for last year, despite the lower year-end 2021 to year-end 2022 loan growth.

Meanwhile, deposits will likely grow mostly in line with loans for the last three quarters of 2022. The following table shows my balance sheet estimates.

| FY17 | FY18 | FY19 | FY20 | FY21 | FY22E | ||||

| Financial Position | |||||||||

| Net Loans | 12,935 | 13,346 | 13,635 | 17,356 | 17,808 | 18,868 | |||

| Growth of Net Loans | 26.0% | 3.2% | 2.2% | 27.3% | 2.6% | 6.0% | |||

| Other Earning Assets | 3,807 | 3,626 | 3,710 | 5,817 | 8,275 | 8,077 | |||

| Deposits | 13,831 | 13,995 | 13,852 | 20,585 | 23,350 | 24,366 | |||

| Borrowings and Sub-Debt | 1,825 | 1,827 | 2,213 | 1,007 | 946 | 990 | |||

| Common equity | 3,241 | 3,252 | 3,364 | 4,298 | 4,718 | 4,862 | |||

| Book Value Per Share ($) | 33.1 | 31.2 | 33.0 | 33.2 | 36.4 | 35.6 | |||

| Tangible BVPS ($) | 18.0 | 17.0 | 18.5 | 19.3 | 21.9 | 21.8 | |||

|

Source: SEC Filings, Author’s Estimates (In USD million unless otherwise specified) |

|||||||||

Margin is Barely Sensitive to Interest Rate Hikes

United Bankshares’ real-estate-heavy loan portfolio is not too sensitive to rate changes. This is because by nature most real estate loans, be they residential or owner-occupied commercial, are usually based on fixed rates. Fortunately, the liability side is also not very sensitive to rate hikes. A sizable 38% of deposits were non-interest bearing at the end of March 2022, as mentioned in the earnings presentation. These deposits will hold back the average deposit costs as interest rates rise. The combination of the asset and liability characteristics leaves the overall balance sheet barely asset-sensitive. The management’s interest-rate sensitivity analysis given in the 10-Q filing shows that a 200-basis points hike in interest rates could boost the net interest income by only 1.4% over twelve months.

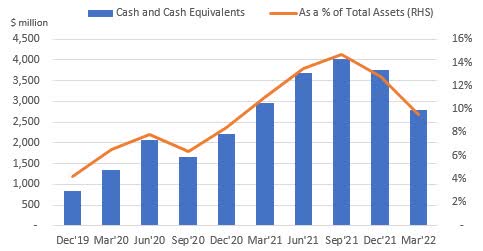

On the plus side, United Bankshares has a large cash balance that will benefit from the significant shift in the short end of the yield curve.

SEC Filings

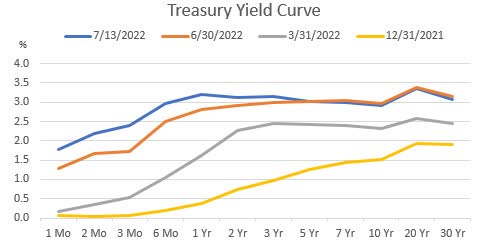

The U.S. Treasury Department

United Bankshares can improve its margin even further by deploying some of the excess cash into higher-yielding assets. Considering these factors, I’m expecting the margin to increase by 14 basis points in the last nine months of 2022 from 2.99% in the first quarter of the year.

Recessionary Threats to Require Higher Provisioning

United Bankshares surprised me by reporting a large provision reversal for the first quarter of the year. Nonperforming loans made up 0.43% of total loans, while allowances made up 1.17% of total loans at the end of March 2022, as mentioned in the presentation. The allowance coverage appeared comfortable at the end of March, but now it’s a little tight considering the threats of a recession. The recent inversion of the yield curve has increased the chances of a recession (see the middle part of the yield curve graph above). Further, the interest rate outlook is now more hawkish than before, which is bad news for asset quality.

Considering these factors, I’m expecting the provision expense to return to a normal level for the last three quarters of the year. However, combined with the first quarter of the year, the provisioning for the full year will likely be below normal. I’m expecting the net provision expense to make up 0.11% of total loans in 2022. In comparison, the provision expense averaged 0.18% of total loans from 2017 to 2019.

Expecting Earnings to Dip by 12%

The anticipated decline in mortgage banking income and provision normalization will likely drag earnings on a year-over-year basis. On the other hand, mid-single digit loan growth and some margin expansion will support the bottom line. Overall, I’m expecting the company to report earnings of $2.50 per share for 2022, down 11.9% year-over-year. The following table shows my income statement estimates.

| FY17 | FY18 | FY19 | FY20 | FY21E | FY22E | ||||

| Income Statement | |||||||||

| Net interest income | 549 | 589 | 578 | 690 | 743 | 803 | |||

| Provision for loan losses | 28 | 22 | 21 | 107 | (24) | 21 | |||

| Non-interest income | 132 | 129 | 150 | 355 | 278 | 205 | |||

| Non-interest expense | 367 | 368 | 383 | 578 | 582 | 561 | |||

| Net income – Common Sh. | 151 | 256 | 260 | 288 | 367 | 340 | |||

| EPS – Diluted ($) | 1.54 | 2.46 | 2.55 | 2.40 | 2.83 | 2.50 | |||

|

Source: SEC Filings, Author’s Estimates (In USD million unless otherwise specified) |

|||||||||

In my last report on United Bankshares, I estimated earnings of $2.54 per share for 2022. I have now tweaked downwards my earnings estimate mostly because I’ve revised downwards the noninterest income estimate for the year.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, the threat of a recession can increase the provisioning for expected loan losses beyond my expectation.

Current Market Price is Close to the Year-End Target Price

United Bankshares is offering a dividend yield of 4.2% at the current quarterly dividend rate of $0.36 per share. The earnings and dividend estimates suggest a payout ratio of 58% for 2022, which is in line with the five-year average of 61%. Therefore, the earnings outlook presents no threats to the dividend level.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value United Bankshares. The stock has traded at an average P/TB ratio of 1.82x in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| T. Book Value per Share | 17.0 | 18.5 | 19.3 | 21.9 | ||

| Average Market Price ($) | 35.9 | 37.3 | 28.1 | 36.9 | ||

| Historical P/TB | 2.11x | 2.02x | 1.45x | 1.69x | 1.82x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/TB multiple with the forecast tangible book value per share of $21.8 gives a target price of $39.6 for the end of 2022. This price target implies a 14.8% upside from the July 13 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 1.62x | 1.72x | 1.82x | 1.92x | 2.02x |

| TBVPS – Dec 2022 ($) | 21.8 | 21.8 | 21.8 | 21.8 | 21.8 |

| Target Price ($) | 35.3 | 37.4 | 39.6 | 41.8 | 44.0 |

| Market Price ($) | 34.5 | 34.5 | 34.5 | 34.5 | 34.5 |

| Upside/(Downside) | 2.2% | 8.5% | 14.8% | 21.1% | 27.4% |

| Source: Author’s Estimates |

The stock has traded at an average P/E ratio of around 13.5x in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| Earnings per Share | 2.46 | 2.55 | 2.40 | 2.83 | ||

| Average Market Price ($) | 35.9 | 37.3 | 28.1 | 36.9 | ||

| Historical P/E | 14.6x | 14.6x | 11.7x | 13.0x | 13.5x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/E multiple with the forecast earnings per share of $2.50 gives a target price of $33.7 for the end of 2022. This price target implies a 2.4% downside from the July 13 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 11.5x | 12.5x | 13.5x | 14.5x | 15.5x |

| EPS 2022 ($) | 2.50 | 2.50 | 2.50 | 2.50 | 2.50 |

| Target Price ($) | 28.7 | 31.2 | 33.7 | 36.2 | 38.7 |

| Market Price ($) | 34.5 | 34.5 | 34.5 | 34.5 | 34.5 |

| Upside/(Downside) | (16.9)% | (9.6)% | (2.4)% | 4.8% | 12.1% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $36.7, which implies a 6.2% upside from the current market price. Adding the forward dividend yield gives a total expected return of 10.4%. As this expected return is not high enough for me, I’m maintaining a hold rating on United Bankshares.

More Stories

Five things to know before applying

Tony Finau wins Rocket Mortgage Classic

2022 Rocket Mortgage prize money payouts for each PGA Tour player