This posting is an on-internet site variation of our Unhedged newsletter. Sign up listed here to get the e-newsletter sent straight to your inbox every weekday

Excellent early morning. We have been pessimistic about China. But not pessimistic ample, as you will see under. We are getting tomorrow off as Rob flies to London and Ethan is effective on non-Unhedged assignments. We’re again with you Thursday. E mail us: [email protected] and [email protected].

China advancement: worse

The final time we wrote about China, at the conclude of very last thirty day period, the subject was the country’s “impossible trilemma”. Fixing at the same time for 5.5 for every cent economic advancement, a steady credit card debt-to-GDP ratio, and zero Covid-19 is unachievable. Given this, the quick-term path of least political resistance for Beijing is supporting growth by pouring credit card debt into reduced-productivity actual estate/infrastructure assignments. Current noises from Xi Jinping make it distinct that the country designs to just take the straightforward path once more.

But it turns out that describing the predicament as a trilemma is too generous. Horrific financial data from China in April suggests that the zero-Covid coverage may perhaps be inconsistent with nearly anything but meagre progress, even in the presence of authorities makes an attempt at stimulus.

Listed here is what April looked like in China:

-

Retail gross sales down 11 for every cent from a yr before, versus an envisioned decline of much less than 7 for each cent.

-

Industrial production dropped 2.9 per cent.

-

Producing was particularly weak, with vehicle creation slipping 41 for every cent.

-

Export progress was 4 per cent, a screeching slowdown from 15 for each cent advancement in March.

-

Authentic estate exercise collapsed, with development starts off falling 44 (!) per cent

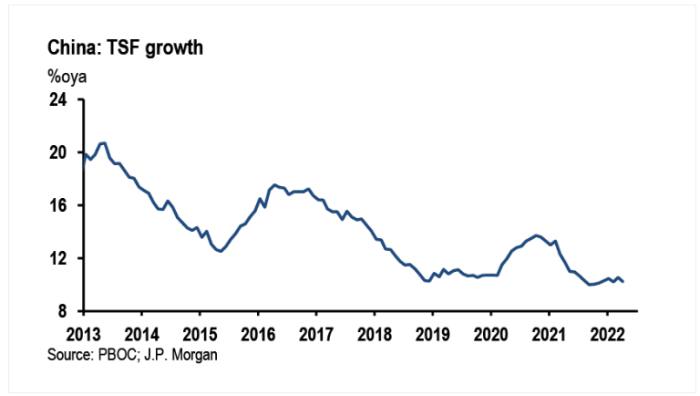

The backdrop for all this is credit history progress that stubbornly refuses to speed up, regardless of plan tweaks (these types of as past months reduction of banks’ reserve prerequisites) and jawboning from the authorities. In this article is a JPMorgan chart of whole social funding (TSF) — a wide govt evaluate of credit rating generation — through April:

JPMorgan’s Haibin Zhu breaks the sideways pattern into three items:

(1) contraction in domestic loans, as marketplace information suggest additional deceleration in house sales (2) noteworthy slowing in medium to long-expression loans to the company sector, reflecting weak credit history demand from customers for company sector financing and expenditure (3) moderation in federal government bond issuance.

Number 1 speaks for alone. China’s genuine estate market is going through a wholesale restructuring. Homebuyers are likely to be treading carefully.

As for selection 2, the key phrase is “demand”. Why would a corporation want to chance a massive new investment, even if lender funding have been available, when the zero-Covid plan has an approximated 300mn town dwellers less than some kind of lockdown. How do we know it is a demand from customers concern? Zhu pointed out “the discrepancy concerning choose up in M2 [broad money] growth . . . and slowdown in personal loan growth . . . Accordingly, the ratio of new loans to new deposits fell to 86.2 for every cent.” Which is the cheapest ratio in 5 decades.

And so we switch to governing administration bond issuance, the go-to when the federal government needs to make some growth. But there is a nasty issue there as effectively, as my colleagues Solar Yu and Tom Mitchell pointed out in an outstanding attribute final week. Nearby government funding autos, a important funding conduit for infrastructure tasks, are experiencing constricted obtain to bank credit score:

Bond issuance by LGFVs was just Rmb758bn ($112bn) over the initial 4 months of this yr, down almost 25 for every cent from the same interval in 2021. Numerous Chinese banks now desire to lend to infrastructure assignments led by substantial point out-owned enterprises rather than LGFVs, which they see as also risky.

The govt will possibly keep hoping to leap-get started points. About the weekend, for instance, the mortgage price for initial-time prospective buyers was slice. But while a number of months back brokers and pundits held out hope for a fillip from authorities action, there is now expanding pessimism about how substantially in can help though the lockdowns are in place. Gavekal Dragonomics pointed out there is “a elementary rigidity involving preserving the recent Covid avoidance strategy and lifting growth”, which renders fiscal stimulus ever more impotent — as demonstrated by lower infrastructure investment in April.

This quotation from the FT understates the level properly:

Zhiwei Zhang, chief economist at Pinpoint Asset Management, famous that the government was beneath tension to start new stimulus steps and that the property finance loan level reduce was “one step in that direction”. But he extra that “the usefulness of these insurance policies depends on how the govt will ‘fine-tune’ the zero-tolerance coverage versus the Omicron crisis”.

High-quality-tune! People today don’t obtain new properties when they are locked in their aged types, and enterprises never borrow when source chains are shut down. Will the federal government relent on zero Covid? No one appears to feel so. In this article is the spectacularly depressing indication-off estimate from Yu and Mitchell’s piece:

Several expect Xi to relax his zero-Covid marketing campaign ahead of securing an unparalleled 3rd expression in electric power at a party congress afterwards this calendar year. The approach “has turn out to be a political campaign — a political resource to exam the loyalty of officials”, says Henry Gao, a China skilled at Singapore Administration College. “That’s considerably more essential to Xi than a couple much more digits of GDP progress.”

Both of those fairness and credit score markets in China capture this grim truth:

However, just one way or a different, quicker or afterwards, the lockdowns will conclude. And there are some signals that the present wave of bacterial infections could be subsiding. Bloomberg reported on Sunday that complete cases in Shanghai were being slipping, and that no new conditions had been documented outside the house of the city’s quarantine locations in two times — nearing a important threshold from calming lockdown protocols.

This kind of detail is sufficient to bring out the optimists. JPMorgan’s China fairness method group has rolled out a record of stocks that will “benefit [from] the Shanghai reopening theme”. They include transportation, semiconductor, car sections, and making resources companies. On the lookout at the price chart earlier mentioned, it is pretty crystal clear that whoever instances the reopening trade just proper is going to make some money in these sorts of names. We wish them well, but wouldn’t know how to time it ourselves.

What kind of development amount China’s economic climate returns to is a individual problem. Julian Evans-Pritchard of Money Economics argued the essential variables will be world-wide need and the want of the governing administration to promote just after the lockdowns are lifted. He foresees a restoration that begins really shortly, but wrote that:

This recovery is possible to be extra tepid than the rebound from the first outbreak in 2020. Back again then, Chinese exporters benefited from a surge in desire for electronics and purchaser products. In contrast, the pandemic-induced shift in spending designs is now reversing, weighing on desire for Chinese exports. In the meantime, officials are using a additional restrained method to policy guidance this time . . . The upshot is that while the worst is with any luck , in excess of, we consider China’s financial state will wrestle to return to its pre-pandemic pattern.

We concur with Evans-Pritchard about worldwide desire but disagree about government restraint. Our guess — and that’s the only term for it, admittedly — is that the futility of stimulus underneath lockdown will only boost the political essential for fiscal and financial largesse right after lockdowns end.

1 superior go through

Depressing illustration of how capitalism functions: the e-pimps of OnlyFans.

More Stories

Five things to know before applying

Tony Finau wins Rocket Mortgage Classic

2022 Rocket Mortgage prize money payouts for each PGA Tour player