Mark Sibson/iStock via Getty Images

Over recent months, there has been a sharp decline across financial markets in the face of growing recession signals. This trend has accelerated in recent weeks as nearly all assets, including stocks and bonds, have experienced rapid declines. While almost all equity sectors have declined, technology and, more recently, financials are faring worst.

The housing and mortgage markets are exciting today since they traversed from a strong boom to a bust over a very short period. When the Federal Reserve began to purchase mortgage-backed securities two years ago, mortgage rates declined to extreme lows and caused the housing market to soar. Conversely, when those purchases ended, mortgage rates soared, causing the housing market to slow. Mortgage lenders, specifically mortgage REITs, are facing extreme declines.

A year ago, when many were fawning mortgage REITs for their high yields, I was one of the few analysts to signal the alarm bells. This view is mainly related to agency-oriented mREITs such as (NASDAQ:AGNC) as detailed in “AGNC: Rising Mortgage Spread Signals Trouble For Agency REITs.” Most mREITs with significant agency mortgage-backed-security assets or “MBS” carry high exposure to the “mortgage spread” or the difference between a mortgage and Treasury interest rates. My view at the time was that as the Federal Reserve began to slow and end MBS purchases, mortgage rates would spike and cause the spread to return to normal levels, causing AGNC’s book value to decline by “20-40%.”

Since then, the mortgage spread has normalized, and AGNC’s price has declined by 40%. AGNC is now at the end of my previous target range. Still, the overall situation has shifted as the extreme spike in energy costs and mortgage rates are pushing the economy into a recession. Based on an ample supply of recent data regarding both banks and the property market, a technical recession is my base case outlook, with a significant slowdown not unlikely. Undoubtedly, this makes a difficult situation worse for AGNC is the mortgage-backed-security market has a habit of freezing when risk perception rises. In my view, this may potentially cause AGNC and its peers to experience a wave of forced asset sales.

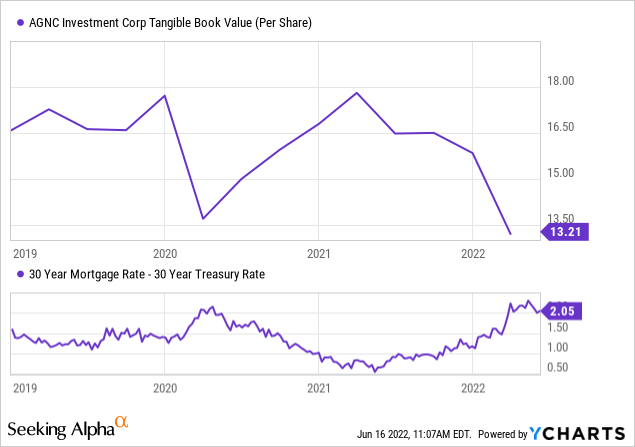

AGNC’s NAV Volatility Is Growing With Rates

Like most MBS-oriented mREITs, AGNC’s business model is relatively simple – buy low-yielding mortgage-backed securities and amplify their yield by using significant leverage. As of Q1, the vast majority of AGNC’s portfolio (over 90%) was made up of 30-year fixed residential agency mortgage-backed-securities. These are large pools of traditional long-term fixed-rate mortgages guaranteed by housing agencies such as Fannie Mae (OTCQB:FNMA) and Freddie Mac (OTCQB:FMCC). Fannie and Freddie make up the difference if borrowers do not meet payments.

This guarantee gives agency MBS assets low credit risk, meaning their yields are often not far above that of the U.S. Treasury. Still, considering Fannie and Freddie do not have a great track record in the event of broad housing market declines (see 2008), the difference in yields between mortgages and Treasuries tends to widen as risk grows. While higher mortgage rates could boost AGNC’s income in the long term, it can also cause its book value to collapse in the short term due to its 7.8X leverage on tangible net book value. See the close inverse relationship below:

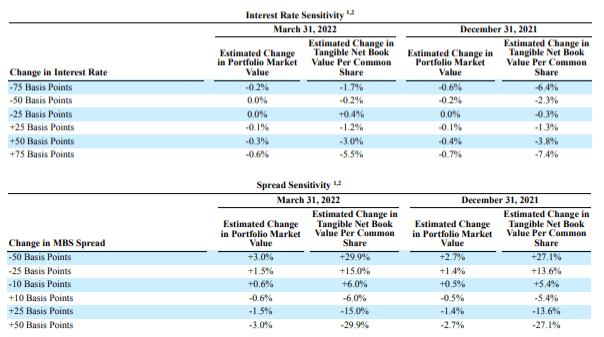

At the end of the last quarter, AGNC had a tangible book value of $13.21. At that time, the base 30-year fixed mortgage rate was around 4.67%, while the 30-year U.S. Treasury rate was 2.44%. The difference between the two, the mortgage spread, was 2.23%. In the company’s last quarterly filing, they reported a mortgage rate spread sensitivity and interest rate sensitivity shown below:

AGNC Q1 2022 Interest Rate Sensitivity Tables (AGNC Q1 2022 10-Q)

A 50 bps (half percent) rise in the mortgage spread is expected to cause AGNC’s book value to decline by roughly 30%. Notably, the mortgage spread had widened dramatically by ~30 bps over the week before the end of Q1 and by ~50 bps from March 15th-31st. Since it may take time for AGNC’s MBS assets and many interest rate hedges to re-value, the company’s reported book value may not have fully considered the recent shock.

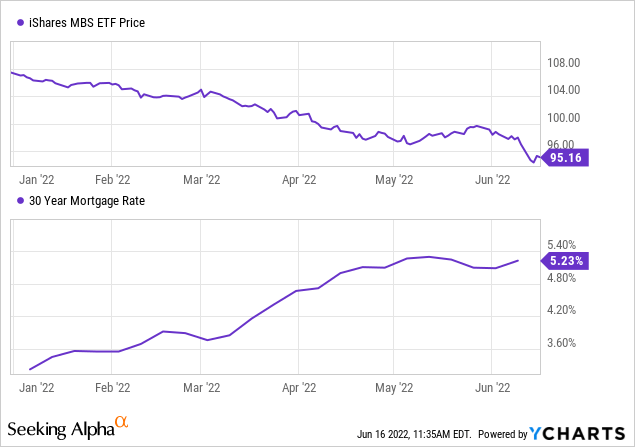

Still, as of the last data, the base 30-year mortgage rate was much higher at 5.23%, with the Treasury rate currently (as of writing) at 3.37%. The spread between the two is slightly lower at 1.86%, potentially benefiting AGNC’s book value. However, mortgage rates are published on a weekly basis while Treasuries are daily, and this week’s massive decline in the agency MBS ETF (MBB) implies the spread has risen sharply higher. See below:

The mortgage rate data is also lagging since it is not based on live market prices, as is the MBS ETF. However, given the relationship between the MBS ETF (MBB) and mortgage rates, I estimate this week’s 30-year base mortgage rate is likely closer to 5.7% today and potentially slightly higher. This increases the estimated spread to 2.33% (5.7% minus 3.37%). A recent survey also suggests mortgage rates of around 5.7% to 5.8%.

Overall, there has been a slight increase in the MBS spread from the end of Q1 to today as of the time of writing. That point is important since the market is extremely volatile today, and as both mortgage rates and Treasuries rise, their potential daily change does as well. Lately, we’re seeing significant rapid 15-30 bps rises and declines in the mortgage spread, which means that AGNC’s net asset value is likely swinging by 5-15% on any given week.

Since the end of Q1, Treasury rates have risen by around 1%, potentially pushing AGNC’s book value around 8% lower (given its -5.5% B.V. exposure to a 75 bps increase in Treasury rates). On the other hand, mortgage spreads are likely around 10-20 bps higher than when AGNC valued its portfolio, implying an additional ~15% in book value. The combined 23% expected decline brings AGNC’s estimated NAV per share to $10.17 (23% below $13.21), almost exactly where the stock is today.

AGNC Best Avoided – MBS Liquidity Concerns

Based on my rate estimates, AGNC may be trading almost precisely at its current estimated net asset value per share. The company also has a 13.5% yield, and as long as Fannie and Freddie can continue to make ends meet, some of that income should remain. Of course, AGNC is borrowing under short-term repurchase agreements, which carried a borrowing rate of 0.37% last quarter. Today, after the recent Fed hikes, that borrowing rate is around 1.5% to 1.75%, so AGNC’s profit margins are under pressure. Over the coming months, I expect this factor to result in a dividend cut, particularly considering the Fed funds rate may be around 3.5% to 4% by year-end.

Considering the expected decline in AGNC’s profit margin and its significant and growing NAV volatility, I believe the stock is best avoided. In 2020, as the spiraling economic outlook led to sharp declines in market liquidity, MBS assets plummeted in value. Virtually all MBS mREITs are subject to tight covenants due to their high leverage, causing many to experience a sharp wave in margin calls during March of 2020.

Most mREITs, including AGNC, have slightly decreased leverage levels, but the potential for a repeat scenario seems to be growing by the day. Last week, the MBS market went ‘no-bid’ as the high CPI data caused the market to unwind. While not entirely related, I use the floating rate ETF (FLOT) as an indicator of financial market liquidity. That fund has plummeted at a relatively extreme pace over the past week and a half – indicating banks and other large investors are rushing for liquidity.

In my view, this creates a material probability that the mortgage-backed-securities market may soon see a larger shock. Unlike in 2020, due to inflation, the Federal Reserve will not be able to quickly rush in to save the market. In my view, if it were not for the Fed’s massive $2T MBS buying program, most mREITs, including AGNC, would not be solvent today. Indeed, such actions from the Fed may have only delayed the inevitable or even worsened the issue by causing home prices to inflate artificially (due to the extreme drop in mortgage rates during MBS Q.E.).

Overall, I am bearish on AGNC and believe it is a very risky bet in today’s volatile market. The mortgage spread is now slightly above its long-term levels, so my bearish thesis on AGNC from last year has now played out. If home prices begin to tumble (which I expect) as unemployment rises (which it may be), then there will be an enormous potential strain on these agencies. Recent rule changes make it so taxpayers cannot easily bail out the agencies. Considering they carry ~$6T in obligations with a leverage of 140 to 1. In my view, the potential repeat failure of these institutions is perhaps the most prominent potential negative catalyst for AGNC, and its peer Annaly (NLY), going forward.

More Stories

Five things to know before applying

Tony Finau wins Rocket Mortgage Classic

2022 Rocket Mortgage prize money payouts for each PGA Tour player