There are some issues you can count on to appear in a Federal Election campaign – climate change, taxes, superior-velocity rail, and the matter of this distinct wire – housing reform.

The very last 7 days of the election campaign has noticed the rebirth of a controversial plan evaluate that could make it possible for young persons to entry their superannuation balances as an support to invest in their 1st home.

Nevertheless, a variety of pundits, analysts, and even tremendous funds have previously known as out the solution (all over again) saying that dwelling costs will increase if the plan goes by – and not on a one-for-1 basis either. Not least impartial economist Saul Eslake who explained on LinkedIn this 7 days that the coverage will be “greeted with despair”.

Does any one find out, Saul notes?

Even Senator Jane Hume (VIC) instructed Radio Nationwide that the coverage will admittedly lead to a “bump” in the value to get a dwelling.

In contrast, Labor is proposing an equally radical and controversial concept – allow the government get a stake in your home, which could be as a great deal as 40% for new homes. When that house is sold down the line, the exact proportion will be taken out of the advertising price tag from your just take-out complete.

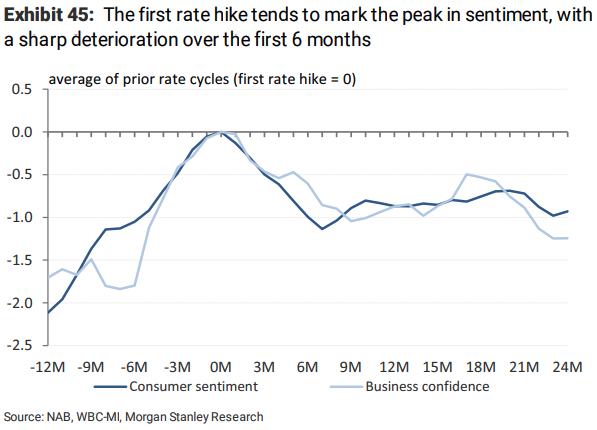

Either way, future property prospective buyers are previously using detect – as this Morgan Stanley chart demonstrates.

Recall, we are just talking about the expense of acquiring a dwelling. We haven’t even began on all the other taxes and payments which occur with it!

An business perspective

The industry see on the use of superannuation in acquiring your have home is clear – don’t do it. Business Tremendous investigation predicts that residence price ranges will go up if the policy is carried out – whether you use the plan or not.

A 30-yr-old on the median wage with a $20,000 setting up equilibrium could be among $14,700-$29,100 worse off at retirement.

Novel remedies

In among all this, economists are split on how very best to cope with the housing affordability disaster. Like Peter Tulip of the Centre of Unbiased Scientific tests, some argue that the remedy is source and desire. Some estimates set the housing shortfall at 160,000+ by 2032 as the inhabitants traits renormalise and worldwide migrants return to our shores.

Other folks have proposed much more abnormal solutions which include the generation of a national housing developer or even a lot more initiatives to generate a lot more social housing. Both way, a ton of shrewd observers have arrive to the exact summary – housing “reform” typically resembles more of a band-assist alternatively than surgery.

While I am flawlessly conscious all those are not comforting words primarily when the RBA’s possess exploration exhibits the financial debt to choose on house prices is looking messy at finest, shocking at worst.

So what is the respond to? This wire will acquire a search at some of the options on the desk, and most importantly, regardless of whether any of them are reasonable.

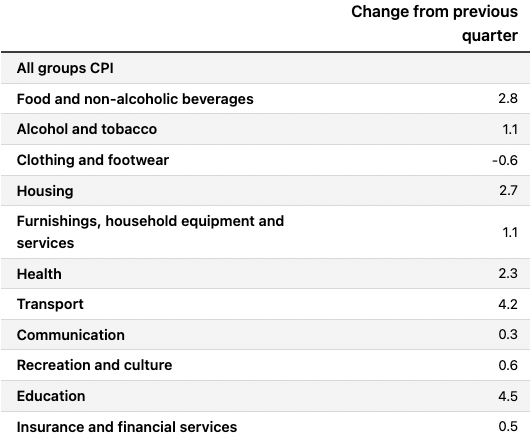

If you want to chat about inflation, you have to converse about housing

In an email discussion I experienced with Damien Klassen of Nucleus Prosperity this week, I was essentially reminded of an critical stage. The most sizeable, main impact on inflation in Australia is truly housing as this desk reveals:

Damien states he has no trouble with the introduction of a super-for-housing plan but he does imagine that it would not handle the crux of the difficulty.

“Do I have a difficulty with employing super? Not really. Except that housing currently has a raft of tax breaks, and superannuation is nonetheless a different tax break. And so, it will be doubling down even more on tax breaks for property,” Damien states.

“Equally functions want to enable house owners buy, neither is helping to reduce the ongoing expense,” Damien provides.

Unsurprisingly, Damien firmly believes climbing rates will be the greatest situation for housing affordability. With the ratio of home loan payments to lease presently at history highs, Damien argues that buyers are heading to get started realising that paying additional than 2 times as considerably a month on your property finance loan repayment than a rental assets just won’t slash it.

Putting all your eggs in a single basket

For investors, the way you may possibly most very likely think about owning further properties is as a hedge towards inflation. Louis Christopher from SQM Investigation states it likely is not going to be diverse in this cycle.

“Authentic estate has historically been perceived as an acceptable hedge versus inflation and I feel the local community will search to serious estate after extra if the RBA fails to tame inflation,” Louis claims.

Like Damien, Louis believes we are not addressing the main section of the challenge. He thinks using superannuation will not dampen rates in the medium to extended run – in actuality, give it one more 12 months and if this policy receives up without the need of a recession, selling prices could be back on the increase by the close of subsequent yr! Additional, dipping into your retirement fund would only increase your individual finance focus risk.

“Possessing close to practically fifty percent of one’s superannuation in a house breaks the recognised gains of asset course diversification and possibly places a considerable volume of one’s retirement price savings at threat of a important housing downturn on an asset that is generally very geared to start with.”

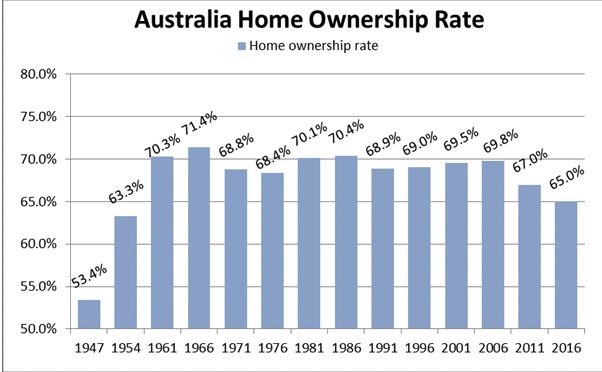

Chart of the 7 days: who needs to have a dwelling?

Louis also handed on a chart that I discover fascinating. It is a steady and gradual drop in homeownership in Australia based on our countrywide census.

The issue that Louis is seeking to make is that no matter the grant, subsidy, program, or in truth policy measure, there is no evidence that any of these schemes have actually experienced an result on homeownership charges. There is certainly been no hindrance (aside from soaring price ranges) but the possibilities placed on the table don’t precisely assist either.

Summary

At the conclude of all this, a single of these two options will conclude up turning into the official solution to our housing crisis. Regardless of whether you believe it really is a band-help or the start out of anything better, you cannot argue with how very long we’ve been speaking about this. To establish it, right here is a direct estimate from an short article courting back to June 2010 showcasing economist Harley Dale:

We are seeing a whole lot a lot more discussion about constraints on the offer of new homes, and federal and state governments are beginning to introduce policies to enhance the housing supply. With any luck , we are going to transform a corner.

It really is amusing how the more issues alter, the extra they continue to be the identical… sadly.

More Stories

Five things to know before applying

Tony Finau wins Rocket Mortgage Classic

2022 Rocket Mortgage prize money payouts for each PGA Tour player